Table of Contents

Executive Summary

A major question for the upcoming review of the EU Emission Trading System (ETS) is how to contain costs while ensuring that green investments, specifically in energy-intensive industries, are not choked off. A key concern for both is the relatively slow progress in rolling out Carbon Capture and Storage (CCS) infrastructure and scaling up hydrogen (H2) supply. Compared to more optimistic expectations that arguably prevailed in the past, this could delay investment in abatement technologies and push up ETS prices, which endangers industrial competitiveness and raises carbon-leakage risks. An important policy option to moderate these effects is additional allowance supply from permanent carbon dioxide removal (CDR). Yet it is unclear how high prices could rise and how much additional supply would be needed to level out price increases.

We use the Aurora EU ETS model to analyze this by comparing two scenarios: one where CCS rollout and H2 upscaling is fast (Base Case), and one where it is relatively slow (Restricted Scenario), but additional allowance supply in the form of CDR is integrated into the ETS. The main findings are:

- CDR integration can make up for slow progress in deploying CCS and H2: ETS prices increase by +77 % in the Restricted Scenario with infrastructure delays, but additional CDR supply can level this out and even push prices below the Base Case level of €203/tCO2 in 2030. Because of market anticipation, ETS prices would already be dampened in the short term well before actual integration starts.

- Relatively small volumes of CDR already have a strong effect: Linearly phasing in CDR by 2035, up to a maximum of 40 MtCO2/yr from 2039 onwards, contains the ETS price increase due to infrastructure delays to +27 % (a reduction of 50 percentage points). Starting in 2030 already and going up to 80 MtCO2/yr by 2039 fully offsets the price increase (+0 %).

- CDR price dampening is likely to be cost-effective: Bringing ETS prices back to Base Case levels (€203/tCO2 in 2030 and €353/tCO2 in 2040) is cost-effective as long as marginal CDR costs do not exceed the corresponding Base Case price in each year. This falls into the range of estimates for future costs, in particular for biogenic emissions capture with carbon storage (BECCS) and biochar carbon removal (BCR).

- CDR integration offers breathing room for the Chemicals sector: In the Restricted Scenario, limited CCS infrastructure and constrained access to low-cost H2 leave the Chemicals sector with fewer viable abatement options, while other sectors (notably Cement) face even tighter constraints. CDR integration restores – and even expands – the Chemicals sector’s room to maneuver, allowing residual emissions of up to 25 Mt in 2040 and beyond.

The modelling excluded several policy options that could substantially affect results, and thus require consideration for deriving broader policy recommendations:

- Using ETS revenues more effectively for industry decarbonization: Currently only a small share (<5 %) of ETS revenues have been used to support industry decarbonization, including acceleration of CCS roll-out and H2 upscaling. Increasing the revenue share to that end is an important option to dampen ETS prices by enabling and incentivizing investment in abatement technologies – resembling the assumptions of the Base Case scenario.

- International credits and additional allowances are potential but risky fallbacks for CDR: If future supply of CDR is insufficient, additional supply could also come from international credits or more EUA allowances. However, these options are riskier in terms of cost-effectiveness, environmental integrity, and governance, and require further analysis. An important precondition for international credits is high integrity ensured through centralized procurement.

- The Market Stability Reserve (MSR) is a suitable docking point for adjusting supply: Adjusting supply is also essential to make the market more resilient to shocks and short-term price volatility. To ensure coherence of the two functions (long-term cost containment and short-term stabilization), the MSR could serve as a docking point under which the rules governing both functions can be unified.

The overall policy recommendation [for the ETS] is to combine supply-side (expanding supply, preferably through CDR integration) and demand-side measures (use auction revenues to support industry decarbonization, accelerating CCS/H2 scale-up). This could contain high ETS prices while simultaneously incentivizing investments in abatement technologies and effectively preventing carbon leakage.

1. Introduction

The EU ETS is entering a structurally different phase. As emissions from the power sector decline rapidly, industrial emissions are becoming the system’s main driver. With fewer abatement opportunities left in electricity generation, ETS prices will increasingly reflect the higher marginal abatement costs of energy intensive industries. At the same time, the cap declines more steeply toward climate neutrality. The combination of a tightening cap and costly industrial decarbonization options will lead to higher ETS prices during the endgame of the 2030s and 2040s (Pahle et al., 2025).

How steeply ETS prices might rise in the 2030s and 2040s will depend strongly on the scale-up of low-carbon industrial transformation options. Next to energy efficiency, electrification and material circularity, availability of CCS and green H2 are the building blocks of industrial decarbonization (ESABCC, 2025). Delays in deploying these technologies leave industries with fewer abatement options precisely as the cap tightens, increasing ETS prices and compliance costs. Across Europe, H2 infrastructure, CCS installations, CO2 transport networks, storage permitting, and investment decisions are progressing more slowly than previously anticipated (European Commission, 2024; Lambert et al., 2024; Odenweller & Ueckerdt, 2025). This creates a direct policy dilemma: excessive price increases could threaten industrial competitiveness and raise carbon-leakage risks, while relaxing the cap would weaken the integrity of the ETS and endanger climate targets.

Permanent CDR is increasingly discussed as a potential “safety valve” because, in principle, it can limit long-term ETS prices while preserving an overall net-zero trajectory (Sultani et al., 2026). In the context of the upcoming ETS review, allowing CDR as a compliance option could therefore help contain price spikes. At the same time, it raises fundamental design and governance questions:

- What is the price effect of delays in the roll-out of CCS/H2 infrastructure?

- To what extent can CDR integration smoothen price spikes, and how do timing and quantity limits affect this outcome?

- Which industrial sectors are most exposed to infrastructure delays, and which sectors benefit most from CDR integration?

- Which policy design elements allow the EU to reap price-stabilization benefits of CDR while avoiding downsides?

2. Model Set-Up and Scenario Design

The analysis is based on the Aurora EU ETS model, which integrates the EU power sector and key industrial abatement options into a single framework, while linking to Aurora global commodity markets and H2 models. The model takes technology options, policy settings, baseline emissions, and commodity prices as inputs and iteratively finds sectoral and temporal equilibria, thereby capturing interdependencies between power and industrial emissions. It represents annual reinvestment and path dependency in technology adoption (e.g., lock-in effects from earlier retrofits and infrastructure availability) and is solved under a perfect-foresight assumption to identify least-cost decarbonization pathways. The model provides sectoral detail for Steel, Cement, Chemicals, and Refining, while aggregating the remaining sectors under “Other Industry”.

All scenarios assume the currently legislated linear reduction factor (LRF) for the EU ETS cap. In line with the 2023 ETS revision, we apply an LRF of 4.3 % per year for 2024-2027 and 4.4 % per year from 2028 onward, including the one-off cap reductions agreed for 2024 and 2026. Under this trajectory, the stationary cap declines towards approximately zero around 2039. The implementation of the MSR reflects legislative provisions as of December 2025, including the rules for allowance intake and the invalidation of certificates held in the MSR.

Substantial carbon leakage would mechanically reduce EUA demand as well as ETS prices. The scenarios therefore assume effective import-related leakage protection through CBAM as well as the avoidance of export-related leakage.

While CDR supply is modelled as exogenous across all sensitivity scenarios, every scenario – including the Base Case and the Restricted Scenario – include limited amounts of endogenous BECCS in the Cement sector in the 2030s and 2040s. To isolate the impact of CCS availability, H2 cost, and CDR on ETS prices, the analysis includes very limited subsidy support, reflecting only support already in place today.

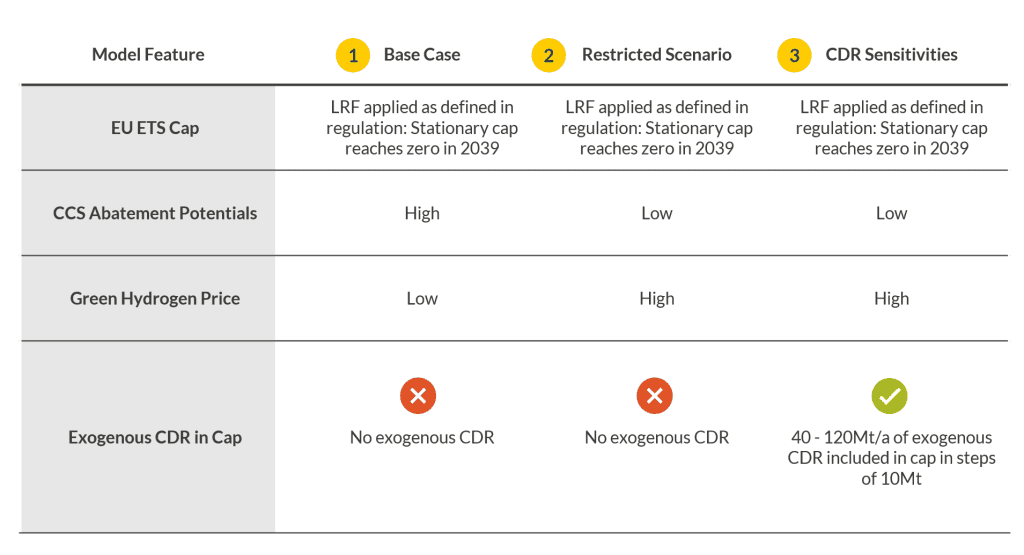

The scenario design proceeds in three steps (Figure 1):

- Base Case. We assume optimistic supply conditions for CCS/H2. Industrial CCS abatement potential ramps up to roughly 300 MtCO2/yr by 2045, and the H2 price follows an optimistic decline, reaching €3.3/kg by 2035 and €2.6/kg by 2045.

- Restricted Scenario. We constrain CCS availability and assume a higher H2 price level, reflecting slower H2 production and pipeline build-out as previously pointed out in the literature. Industrial CCS abatement potential is 45 % lower than in the Base Case by 2040 and 2045, while the H2 price trajectory begins to decline only in 2035 and remains 57 % higher than in the Base Case by 2040 and 2045.

- CDR Sensitivities. Building on the Restricted Scenario, exogenous CDR is added as an annual cap-expansion equivalent. We test annual CDR availability limits between 40 and 120 MtCO2/yr, in 10 Mt increments, with phase-in starting in 2030 and 2035, yielding 18 sensitivity cases in total.

3. Results and Interpretation

3.1 ETS Price Dynamics under Optimistic and Delayed CCS and H2

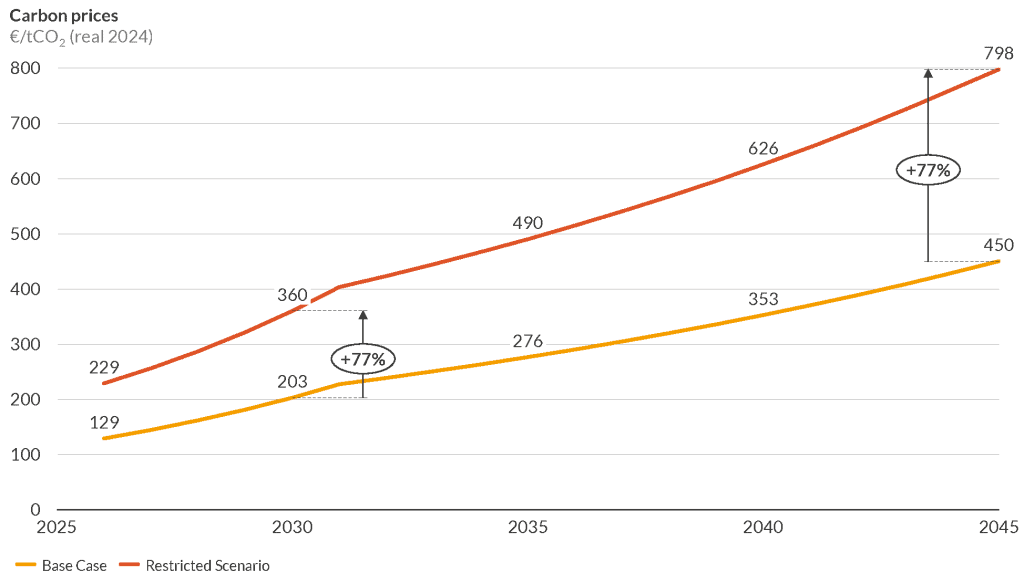

Comparing the Base Case and the Restricted Scenario shows how strongly ETS prices depend on the timely availability of CCS/H2 (Figure 2). In the Base Case, the ETS price reaches €450/tCO2 in 2045. In the Restricted Scenario, abatement options associated with CCS and H2 are scarcer and more expensive, pushing the price close to €800/tCO2 in 2045 – around 77 % above the Base Case. As the cap tightens, scarcity in these infrastructure-dependent options translates into stronger price pressure. Conversely, faster deployment of CCS and H2 would be expected to ease that pressure and lower ETS prices (and should be pursued with priority). However, given the delays already underway, it seems prudent to assess complementary options.

3.2 Required CDR Volumes to Stabilize Prices

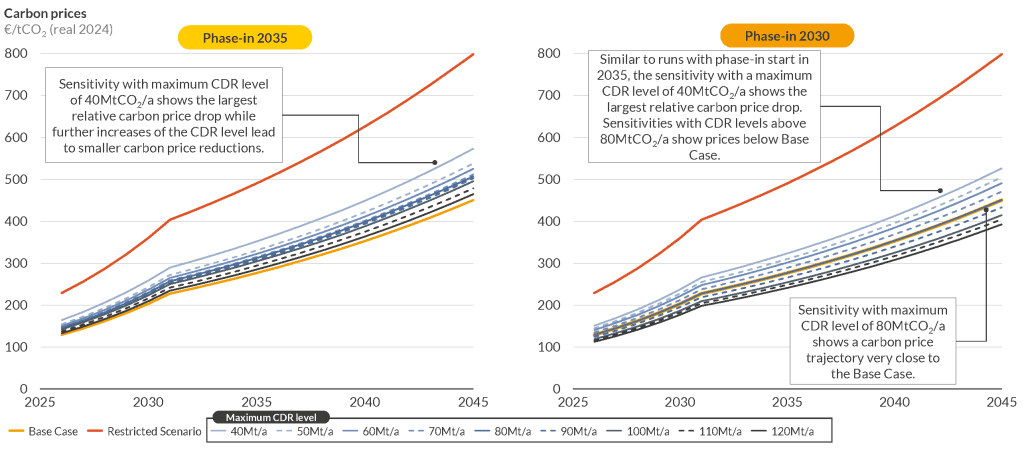

If the industrial sectors face higher decarbonization costs due to broader system delays, a key question is how much eligible CDR would be needed to bring ETS prices back towards the level of the Base Case. While we model the increase in certificate supply through an exogenous cap expansion, our analysis focuses on CDR because providing this supply through removals would keep the ETS ambition at current levels. A cap adjustment through the LRF, on the other hand, would reduce the pace at which ETS sectors achieve net zero. Our approach consequently abstracts from CDR supply curves, but we discuss potential cost effectiveness consideration below. Figure 3 summarizes 18 sensitivity runs for the Restricted Scenario, where exogenous CDR enters as a cap-expansion equivalent: each ton of eligible CDR increases effective allowance supply up to an annual maximum of 40-120 MtCO2/yr, with phase-in years of 2030 or 2035. For example, CDR is assumed to be upscaled from 0 in 2030 to 40 Mt MtCO2/yr in 2039 in the “40 Mt/a” sensitivity with phase-in in 2030.

The CDR sensitivity analysis yields four core messages:

First, price effects occur before formal phase-in. Even when CDR integration only starts in 2035, prices already decline relative to the Restricted Scenario in the late 2020s. The reason is intertemporal optimization: market participants anticipate future allowance supply and adjust banking decisions accordingly.

Second, the price effects of relatively small CDR volumes are already quite substantial. Across both phase-in dates, the first tranche of CDR integration (40 MtCO2/yr) delivers the largest relative price reduction, even though volumes ramp up gradually in the early years. Relative to the Restricted Scenario, 2030 carbon prices are 34 % lower with a 2030 phase-in of the first CDR tranche, and 28 % lower under a 2035 phase-in (relative to the Base Case). Additional CDR further lowers prices, but with diminishing marginal effects.

Third, comparatively modest CDR volumes can move prices substantially. With a 2030 phase-in, around 80 MtCO2/yr in the long run are sufficient to bring the price path back towards the Base Case, and annual limits above 80 MtCO2/yr can even push prices below the Base Case. With a 2035 phase-in, by contrast, prices remain materially above the Base Case through 2040 unless annual CDR volumes move towards the upper end of the tested range.

Fourth, quantity limits matter. Because the additional supply enters under binding quantitative caps, the mechanism does not create a hard price ceiling. Once the annual CDR limit binds, the remaining scarcity is still cleared through conventional abatement, so ETS prices can remain above the implied CDR cost benchmark.

It is important to note that a rapidly tightening ETS cap towards (near-)zero in the endgame, combined with rising volumes of eligible CDR, fundamentally changes the market’s price-setting mechanism. While in earlier phases the ETS price primarily reflects the marginal cost of conventional abatement options, in later phases it increasingly reflects the marginal cost – and scarcity – of eligible CDR.

3.3 Cost-effectiveness of CDR Supply

For CDR to reduce ETS prices cost-effectively, eligible supply must be available at or below the prevailing ETS price. Figure 3 provides indicative ETS price ranges; this translates into approximate CDR cost thresholds of €180-260/tCO2 in 2030 and €300-450/tCO2 in 2040. Meeting these thresholds is a necessary condition for CDR to function as a meaningful price-level stabilizer for the system.

Recent CDR cost projections from the literature are consistent with these expectations – in the case of BECCS already within the coming decade, and increasingly so for DACCS towards 2040. Sultani et al. (2026) project BECCS certificates to be available at €200-300/tCO2 within the EU ETS around 2030. This aligns closely with industry-level cost expectations for BECCS at around €240/tCO2 for the period between 2030 and 2045 (MVV Energie AG, 2025), as well as those by the European Scientific Advisory Board on Climate Change, which estimates BECCS to be available at €150-250/tCO2 (ESABCC, 2025). For DACCS, Sultani et al. (2026) build on cost projections from Sievert et al. (2024) to show that installations in the EU could break even with EU ETS prices from 2040 onwards, reaching €300-350/tCO2 as the technology continues to scale. However, uncertainty remains as literature reviews deem DACCS in the range of $100-600/tCO2 (€85-513/tCO2) as plausible (van der Spek et al., 2025). Should policymakers also choose to integrate BCR – which qualifies as permanent under the EU’s Carbon Removal and Carbon Farming (CRCF) framework (DG CLIMA, 2026) – data points from voluntary markets suggest that high-quality certificates would be available at around €130-150/tCO2 as of today (Canel Soria & Gupta, 2025). For the long term, the literature reports cost ranges of $70-$360/tCO2 (€60-308/tCO2) for BCR (Chiquier et al., 2025).

Current cost projections therefore imply that a supply of CDR certificates at prices compatible with the EU ETS Base Case trajectory is within reach. An open question remains: Will the EU be able to scale the required CDR volumes in the coming decade? While a CDR integration into compliance markets can send an important first signal, additional policy support will be required to have the required volumes available in time (Kozian et al., 2026). One option is for governments to buy initial batches of CDR certificates at a premium, de facto subsidizing early-mover projects through institutional arrangements like a buyer’s coalition (McDonald et al., 2025). While further discussions will therefore be necessary on both early support instruments and required Monitoring, Reporting and Verification (MRV) measures to ensure certificate integrity, the cost dimension in itself does not seem to represent a fundamental barrier to integration.

3.4 Sectoral Outcomes

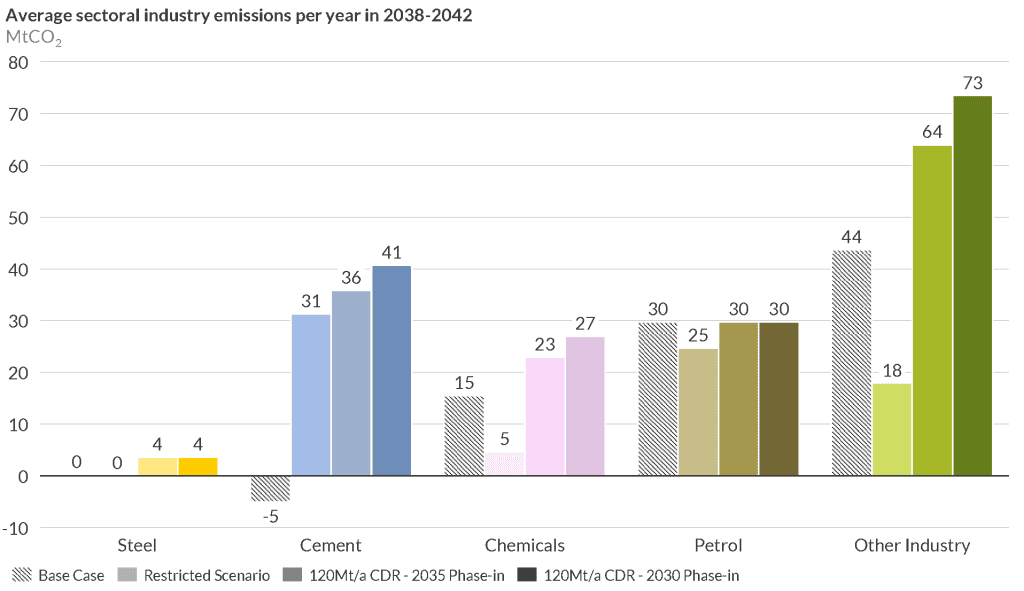

Comparing sector-specific remaining emissions around 2040 between the Base Case, Restricted Scenario and selected CDR sensitivities allows us to disentangle the sectoral impact of restricting abatement options with CCS/H2, as well as the effects of subsequently integrating CDR in this case (Figure 4).

Our results emphasize that the Restricted Scenario requires more abatement from the Chemicals sector and “Other Industry”. An integration of CDR specifically provides “breathing room” for those two sub-sectors, mostly because the limited availability of CCS in the Restricted Scenario results in higher residual emissions from the Cement sector, for which Chemicals and “Other Industry” have to compensate (cf. first two bars in Figure 4 of these three sectors respectively). This breathing room is particularly relevant in light of vocal criticism from the Chemicals industry during the consultations for the 2026 EU ETS review. Whereas, up to 2030, emissions in the model remain broadly similar across scenarios, after 2030 – i.e., once the CCS/ H2 constraints become binding – sectoral pathways diverge. Higher ETS prices generally strengthen incentives for additional abatement, so that emissions fall where viable technical alternatives remain available and cheaper than purchasing allowances. By contrast, in sectors that rely on infrastructure- and feedstock-dependent pathways, constraints translate more directly into higher residual emissions and compliance costs, making these sectors particularly sensitive to delays.

The Cement sector is particularly infrastructure-sensitive: because decarbonization depends on CCS for process emissions (ECRA, 2022), constrained CCS availability generates a persistent emissions delta and correspondingly high incremental compliance costs due to additional EUA purchases at elevated price levels in the Restricted Scenario.

In contrast, the Chemicals sector reacts to the high carbon prices through higher decarbonization of heat via electrification. Although this approach is generally more cost-effective than compensating emissions through the purchase of EUA allowances, the required investments place substantial financial pressure on Chemicals producers. Given the European Chemicals industry’s current competitiveness challenges (Roland Berger, 2025), it remains uncertain whether these investments will be made quickly enough to help contain ETS prices. Allowing a limited deployment of CDR could alleviate this pressure. In this sense, CDR could function as a targeted tool to make the transition more manageable where infrastructure bottlenecks and high abatement costs might otherwise create excessive strain.

4. Further Considerations

4.1 Use of ETS Revenues

ETS revenues should play a stronger role in promoting industrial decarbonization, yet their use remains limited and largely unconditional. In 2024, €24.4 billion accrued to Member States, of which only €0.8 billion (3 %) was used for industrial decarbonization (DG CLIMA, 2025). A further €3.2 billion (13 %) financed compensation for indirect carbon costs, much of which flowed to sectors already reliant on electricity, such as aluminum production.

In Germany, preliminary figures for 2026 show a similar pattern: €2.9 billion (67 %) of €4.3 billion in ETS revenues is allocated to such compensation (hib Meldungen, 2025). Additional funding includes €1.3 billion for hydrogen and €0.7 billion for industrial decarbonization, supplemented by resources from the new “special fund”. While Germany channels a larger share of revenues to industry than the EU average, most of this support is not directly tied to new investment. Instead, it only indirectly incentivizes decarbonization, for example when firms switch from fossil-based production to electrified processes such as electric arc furnaces.

In light of this, an important lever is to implement stricter conditionalities for the use of ETS revenues. The revision of ETS directive 2003/87/EC from 2023 already requires Member States to use 100 % of their revenues for climate-related purposes, with the exception of those used for compensation of indirect carbon costs (see above). The “climate-related” conditionality could be tightened to a certain percentage share that must be used for industry decarbonization, potentially also channeled through the EU Innovation’s Fund “Auctions-as-a-Service”. Also for indirect carbon costs a conditionality already exists: beneficiaries are obliged to (1) conduct an energy audit and implement recommendations, (2) reduce the carbon footprint of their electricity consumption, (3) invest a significant share of at least 50 % of the aid amount in projects that lead to substantial reductions of the installation’s greenhouse gas emissions (European Commission, 2021). It is probably too early to conclude how effective these measures are, but given the large financial volume – especially in Germany – this issue deserves more scrutiny and public debate on how to improve conditionalities over time.

4.2 Article 6 as a Fallback

If the required allowance supply to stabilize ETS prices proves impossible to meet through cost-effective domestic CDR alone, credits according to article 6 of the Paris Agreement (United Nations, 2015) could potentially serve as a fallback option. The EU’s need to engage in the financing of international carbon credits is already widely acknowledged in policy circles (Delbeke, 2026; ESABCC, 2025) and has now been formally incorporated into the EU’s 2040 climate target (EU Council, 2026). In this sense, the question is less whether international credits will play a role in the EU’s climate architecture, but rather under what conditions and through which channels they will do so.

Three key questions remain unresolved. The first concerns which certificate types should be permitted within the EU’s policy framework. Trust in international carbon markets has eroded considerably after the reputational damage from adverse experiences with Kyoto-era credits (Wara, 2007) and the voluntary carbon market (Probst et al., 2024). This makes robust integrity measures for certificates of non-EU origin essential. One initial step in restoring that trust could be to restrict procurement strictly to international (permanent) CDR, excluding offset credits altogether. Second, it remains unclear how the inclusion of Art. 6 credits will impact the external dimension of the EU’s climate policy architecture. Relying on international cooperation requires not only the identification of trusted partners, but also market and capacity building outside the EU’s jurisdiction. To this end, a “pilot period” for international credits as included in the latest EU Climate Law revision could be a useful starting point. The third open question is whether Article 6 credits should be brought into the EU ETS. The domestic price effects of such an integration are inherently uncertain ex-ante and would depend heavily on the types of certificates ultimately permitted.

The use of Article 6 credits could therefore carry greater risks than domestic CDR across the dimensions of cost-effectiveness, certificate quality, and governance. While these risks warrant further analysis, a prerequisite for any integration must be a high and verifiable standard of integrity. One mechanism to achieve this would be centralized public procurement with credible certification, whereby international credits are acquired by a designated public body and only released into the EU ETS following thorough due diligence. Such an approach would allow the EU to retain control over certificate quality while still drawing on international supply when domestic options fall short.

4.3 Integration of CDR through the MSR

Given the many uncertainties surrounding allowance demand, actual future market conditions are likely to substantially deviate from modelled price trajectories. This makes a case for integrating CDR contingent on the contemporaneous state of the market, i.e., its supply-demand balance. Concretely, this means using state-contingent, rule-based supply adjustments to control when and how much CDR enters the market, similar to the functioning of the MSR. The MSR could therefore serve as a docking point for governing CDR integration, for example by linking CDR entry to transparent indicators such as the allowance surplus (TNAC) and/or predefined price or volatility triggers. Operationally, this could take the form of predefined triggers that scale eligible CDR entry up or down when the market moves into scarcity (e.g., high prices/low surplus) and pause entry when conditions normalize. In addition, the MSR would function as a buffer, ensuring that only high-integrity certificates enter the market in times of scarcity (Delbeke, 2026).

A unified, rules-based approach would reduce uncertainty about future ETS price levels and help dampen volatility. It could also avoid unintended interactions between the MSR and LRF, as highlighted by Perino et al. (2022), by placing long-term cost containment and short-term stabilization under a coherent governance framework. A key challenge, however, is that state-contingent entry increases ex ante uncertainty about future CDR demand and volumes, which can weaken investment incentives for CDR supply. Complementary policies would therefore be needed to scale up deployment – for example, by using ETS auction revenues to de-risk early projects and support enabling infrastructure and MRV readiness. The issue of CDR integration through the MSR therefore warrants more consideration and research going forward (Verbist et al., 2025; Pahle et al., forthcoming).

5. Conclusion

The pace of CCS and H2 deployment will be a key determinant of EU ETS price developments in the 2030s and beyond. Under a rapidly tightening cap, delays in these enabling infrastructures are likely to translate into substantially higher and more volatile carbon prices, increasing political resistance and potentially driving industrial actors out of business before they get the opportunity to transform. Against this backdrop, limited exogenous CDR integration can serve as a transitional safety valve. Our results show that even relatively modest CDR volumes can have a strong price effect, and that expectations about future CDR availability may already dampen prices before removals are deployed. At the same time, CDR is not a substitute for industrial decarbonization. Its role should be to ease temporary scarcity due to belated CCS/H2 deployment and reduce adjustment pressure where infrastructure bottlenecks are most acute. This is particularly relevant for hard-to-abate sectors such as Chemicals, where high carbon prices can create disproportionate cost pressure during the transition.

We derive the following policy implications from our analysis: First, auction revenues should be used more strategically to accelerate CCS/H2 deployment and thereby reduce the need for future price-stabilization measures. Second, any integration of CDR should be gradual, limited in volume, and embedded in a credible governance framework, with the MSR as a potential docking point. Third, the most robust approach is to combine both sides of the policy mix: targeted support for industrial decarbonization together with limited flexibility on the supply side. This would help contain excessive ETS price spikes while preserving investment incentives and maintaining the credibility of the EU’s climate targets.

Ariadne-Kurzdossier – deutsche Zusammenfassung

Frank Best, Michael Pahle, Darius Sultani, Claudia Günther, Malte Herten, Jörn Richstein, Ottmar Edenhofer (2026): Ein Sicherheitsventil für die Endphase des EU-Emissionshandelssystems: Preisstabilisierung durch die Entfernung von Kohlendioxid. Kopernikus-Projekt Ariadne, Potsdam.

Literaturangaben

Canel Soria, S., & Gupta, Y. (2025). Biochar carbon credit prices steady, but sentiment weakens. S&P Global. https://www.spglobal.com/energy/en/news-research/latest-news/electric-power/111325-biochar-carbon-credit-prices-steady-but-sentiment-weakens

Chiquier, S., Gurgel, A., Morris, J., Chen, Y.‑H. H., & Paltsev, S. (2025). Integrated assessment of carbon dioxide removal portfolios: Land, energy, and economic trade-offs for climate policy. Environmental Research Letters, 20(2), 24002. https://doi.org/10.1088/1748-9326/ada4c0

Delbeke, J. (2026). Preparing the 2026 EU ETS/MSR review. https://doi.org/10.2870/4771323

DG CLIMA. (2025). Climate action progress report 2025: strengthening competitiveness on the road to climate neutrality. Directorate-General for Climate Action. https://doi.org/10.2834/0963577

DG CLIMA. (2026). EU sets world’s first voluntary standard for permanent carbon removals. Directorate-General for Climate Action. https://climate.ec.europa.eu/news-other-reads/news/eu-sets-worlds-first-voluntary-standard-permanent-carbon-removals-2026-02-03_en

ECRA. (2022). The ECRA Technology Papers 2022 – State of the Art Cement Manufacturing: – Current Technologies and their Future Development. Düsseldorf. European Cement Research Academy. https://ecra-online.org/research/technology-papers

ESABCC. (2025). Scaling up carbon dioxide removals: Recommendations for navigating opportunities and risks in the EU (Publications Office of the European Union). Luxembourg. European Environment Agency. https://doi.org/10.2800/3499931

EU Council. (2026). Regulation (EU) 2026/667 of the European Parliament and of the Council amending Regulation (EU) 2021/1119 as regards the setting of a Union intermediate climate target for 2040. European Parliament and the Council of the European Union.

European Commission. (2021). Guidelines on certain State aid measures in the context of the system for greenhouse gas emission allowance trading post-2021. Official Journal of the European Union. https://eur-lex.europa.eu/eli/guideline/2021/415

European Commission. (2024). Towards an ambitious Industrial Carbon Management for the EU. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=COM:2024:62:FIN

Kozian, A., Ellensohn, J., Schmidt, T. S., & Steffen, B. (2026). A global analysis of expected revenues from carbon dioxide removal. Environmental Research Letters, 21(5), 54015. https://doi.org/10.1088/1748-9326/ae499d

Lambert, M., Barnes, A., Marcu, A., Imbault, O., Bhashyam, A., Tengler, M., Cavallera, C., & Romeo, G. (2024). 2024 State of the European Hydrogen Market Report. https://www.oxfordenergy.org/publications/2024-state-of-the-european-hydrogen-market-report/

McDonald, H., Gardiner, J., Görlach, B., & Tarpey, J. (July 2025). An EU purchasing programme for permanent carbon removals: Assessment of policy options and recommendations for short-term policy design.

MVV Energie AG. (2025). Wege zur Skalierung von Negativ emissionstechnologien: Empfehlungen für Marktdesign, Infrastruktur und Finanzierung. Mannheim. https://www.mvv.de/fileadmin/user_upload/Ueber_uns/de/innovationen/beccus/MVV_Studie_BECCUS_Print.pdf

Odenweller, A., & Ueckerdt, F. (2025). The green hydrogen ambition and implementation gap, 10(1), 110-123. https://doi.org/10.1038/s41560-024-01684-7

Pahle, M., Günther, C., Meus, J., Sultani, D., & Verbist, F. (forthcoming). Integrating CDR into the EU ETS revisited: Intervention logics, institutional docking points & signalling to market.

Pahle, M., Quemin, S., Osorio, S., Günther, C., & Pietzcker, R. (2025). The emerging endgame: The EU ETS on the road towards climate neutrality. Resource and Energy Economics, 81, 101476. https://doi.org/10.1016/j.reseneeco.2024.101476

Perino, G., Willner, M., Quemin, S., & Pahle, M. (2022). The European Union Emissions Trading System Market Stability Reserve: Does It Stabilize or Destabilize the Market? Review of Environmental Economics and Policy, 16(2), 338–345. https://doi.org/10.1086/721015

Probst, B. S., Toetzke, M., Kontoleon, A., Díaz Anadón, L., Minx, J. C., Haya, B. K., Schneider, L., Trotter, P. A., West, T. A. P., Gill-Wiehl, A., & Hoffmann, V. H. (2024). Systematic assessment of the achieved emission reductions of carbon crediting projects. Nature Communications, 15(1), 9562. https://doi.org/10.1038/s41467-024-53645-z

Roland Berger. (2025). European chemical closures and investments radar 2022-2025: Radar report 1 – Commissioned by Cefic. https://cefic.org/resources/european-chemical-closures-investments-radar-2022-2025/

Sievert, K., Schmidt, T. S., & Steffen, B. (2024). Considering technology characteristics to project future costs of direct air capture. Joule, 8(4), 979–999. https://doi.org/10.1016/j.joule.2024.02.005

Sultani, D., Osorio, S., Günther, C., Pahle, M., Sievert, K., Schmidt, T. S., Steffen, B., & Edenhofer, O. (2026). How the EU can utilize its carbon market to scale up carbon dioxide removal. Joule. Advance online publication. https://doi.org/10.1016/j.joule.2026.102395

United Nations. (2015). Paris Agreement. https://unfccc.int/sites/default/files/english_paris_agreement.pdf

van der Spek, M., Bardow, A., Baum, C. M., Bolongaro, V., Dufour-Décieux, V., Esch, C., Fritz, L., Garcia, S., Hamann, C., Hondeborg, D., Kiani, A., Lueck, S., Patel, S. K., Peh, S. B., Pisciotta, M., Psarras, P., Repke, T., Sáenz-Cavazos, P. A., Schulte, I., . . . Minx, J. C. (2025). An ecosystem of carbon dioxide removal reviews – part 1: Direct air CO2 capture and storage. Energy & Environmental Science, 18(22), 9713–9785. https://doi.org/10.1039/D5EE01732G

Verbist, F., Sultani, D., & Pahle, M. (2025). Rules instead of Limits? Taking the CDR Integration Debate to the next Level. Presentation at Ariadne@Brussels. https://ariadneprojekt.de/media/2025/12/9_AriadneInput_Verbist.pdf

Wara, M. (2007). Is the global carbon market working? Nature, 445(7128), 595-596. https://doi.org/10.1038/445595a